Page 112 - 2596-CA SR Lanka- Annual Report 2022

P. 112

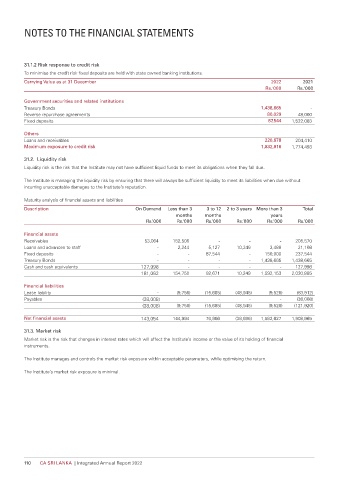

NOTES TO THE FINANCIAL STATEMENTS

31.1.2 Risk response to credit risk

To minimise the credit risk fixed deposits are held with state owned banking institutions.

Carrying Value as at 31 December 2022 2021

Rs.'000 Rs.'000

Government securities and related institutions

Treasury Bonds 1,438,665 -

Reverse repurchase agreements 80,029 48,000

Fixed deposits 87,544 1,522,083

Others

Loans and receivables 226,678 204,410

Maximum exposure to credit risk 1,832,916 1,774,493

31.2. Liquidity risk

Liquidity risk is the risk that the Institute may not have sufficient liquid funds to meet its obligations when they fall due.

The Institute is managing the liquidity risk by ensuring that there will always be sufficient liquidity to meet its liabilities when due without

incurring unacceptable damages to the Institute’s reputation.

Maturity analysis of financial assets and liabilities

Description On Demand Less than 3 3 to 12 2 to 3 years More than 3 Total

months months years

Rs.’000 Rs.’000 Rs.’000 Rs.’000 Rs.’000 Rs.’000

Financial assets

Receivables 53,064 152,506 - - - 205,570

Loans and advances to staff - 2,244 5,127 10,249 3,488 21,108

Fixed deposits - - 87,544 - 150,000 237,544

Treasury Bonds - - - - 1,438,665 1,438,665

Cash and cash equivalents 127,998 - - - - 127,998

181,062 154,750 92,671 10,249 1,592,153 2,030,885

Financial liabilities

Lease liability - (9,756) (15,685) (48,945) (9,526) (83,912)

Payables (38,008) - - - - (38,008)

(38,008) (9,756) (15,685) (48,945) (9,526) (121,920)

Net financial assets 143,054 144,994 76,986 (38,696) 1,582,627 1,908,965

31.3. Market risk

Market risk is the risk that changes in interest rates which will affect the Institute’s income or the value of its holding of financial

instruments.

The Institute manages and controls the market risk exposure within acceptable parameters, while optimising the return.

The Institute’s market risk exposure is minimal.

110 CA SRI LANKA | Integrated Annual Report 2022